The End of Anonymous Gambling: How 2026’s Global Privacy Crackdown Is Reshaping Crypto Casinos

The founding promise of crypto gambling was simple. Play anywhere, with anyone, without a bank knowing about it. Deposit from a wallet. Win or lose. Withdraw back to a wallet. No statement. No record. No questions from your financial institution.

In 2026, that promise is being systematically dismantled. Not by a single regulator with a dramatic announcement, but by a quiet, coordinated global wave of reporting obligations, exchange licensing frameworks, and tax authority data-sharing agreements that are closing the anonymous gambling window from every direction at the same time. The anonymous gambling era is not ending with a ban. It is ending with a spreadsheet.

The Original Promise and Why It Worked

To understand what is being lost, it helps to understand what made crypto gambling genuinely private in its early years.

Bitcoin transactions are pseudonymous. They are recorded publicly on the blockchain, but linked to wallet addresses rather than names. A Bitcoin deposit to a casino address appears on the ledger as a transfer between two strings of characters which readable by anyone, but attributable to no one without additional investigation. For the vast majority of players making recreational deposits, this pseudonymity was functionally indistinguishable from anonymity—and it’s one of the myths about crypto casinos.

The second layer of protection was the on-ramp . Before crypto exchanges became regulated by licensed infrastructure with mandatory Know Your Customer (KYC) verification, buying Bitcoin was genuinely private. Peer-to-peer cash trades, Bitcoin ATMs, and early unregulated exchanges allowed players to acquire crypto without creating any traceable connection between their real identity and their wallet address.

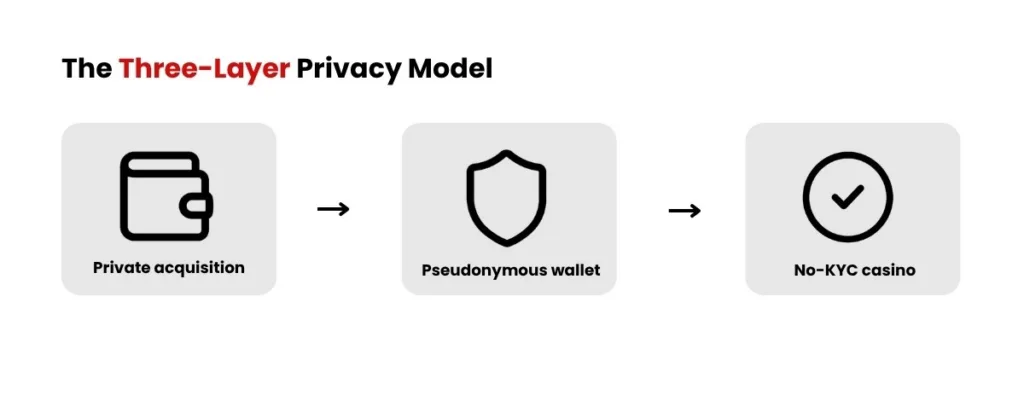

The third layer was the casino itself. Offshore platforms with no domestic licensing obligations had no reason to demand identity verification, and no regulator compelling them to do so. A username, an email address, and a crypto wallet was sufficient.

This three layer structure, private acquisition, pseudonymous blockchain, no-KYC casino, created a genuinely private gambling environment that no traditional payment method could replicate. It worked, and it attracted players who had entirely legitimate reasons for wanting financial privacy alongside those who did not.

Each of those three layers is now under simultaneous attack

Why Players Want Anonymity

Before examining what is being dismantled, it is worth being clear about why players valued this privacy in the first place. The assumption that anonymous gambling is inherently suspicious is not necessarily the case. They are several legitimate reasons why players would want anonymity.

Social stigma is real.

Gambling carries genuine stigma in many cultures, workplaces, and families. A recreational player who spends $50 a week on football betting is engaged in a legal activity, but may reasonably prefer that their employer, partner, or parents not see it itemised on a bank statement.

Banking discrimination has a documented history.

Banks have flagged, restricted, and closed accounts belonging to customers identified as regular gamblers, treating a legal recreational activity as a credit or reputational risk factor. The Irish consumer protection authority, the UK’s Financial Conduct Authority, and consumer advocacy groups in multiple countries have documented cases of banks taking adverse action against customers specifically because of gambling transactions on their statements. Crypto offered an escape from this structural discrimination.

Professional consequences are a genuine concern.

Lawyers, financial advisors, doctors, teachers, and others working in regulated or reputationally sensitive professions can face disciplinary consequences if gambling activity becomes known to employers or professional bodies, even when it is entirely legal and conducted responsibly. A lawyer playing online poker on weekends is breaking no law. They may nonetheless have strong reasons to keep it out of their financial record.

Legal ambiguity creates rational privacy seeking.

In markets like India, the Philippines, and Hong Kong, players accessing offshore platforms occupy genuine legal grey areas. The prohibition in these jurisdictions targets operators rather than individuals, but the law is unclear enough that players have reasonable cause to be cautious. Seeking financial privacy in this context is a rational response to ambiguous law, not evasion of clear prohibition.

KYC data security is a legitimate concern.

Multiple documented cases in 2024 and 2025 involved offshore casino KYC data, identity documents submitted during account verification, being leaked or sold to identity fraud operators on dark web marketplaces. Uploading a government-issued ID to an offshore casino server you know nothing about carries real data security risk that has nothing to do with hiding gambling activity. A player who declines to do so is making a prudent security decision, not concealing criminal activity.

Financial privacy is a recognized civil interest.

It is a principle recognised in democratic societies as a legitimate civil interest. Financial surveillance of legal activity, even when its stated purpose is tax compliance, narrows personal freedom in ways that extend beyond the specific activities being monitored. The argument that only people with something to hide want privacy is as unconvincing in financial contexts as it is in any other.

Financial privacy is not the same thing as criminal secrecy.

Financial privacy is not the same thing as criminal secrecy.

Most anonymous gambling users were ordinary players seeking discretion, security, or protection from unnecessary scrutiny.

None of this means that anonymous gambling is without legitimate concerns. Tax evasion, money laundering, and problem gambling facilitation are genuine issues that privacy tools can complicate. The point is that the population of players who valued anonymous gambling was not primarily composed of bad actors. It was composed of ordinary people with ordinary, legitimate reasons for financial discretion. Understanding that is necessary for an honest assessment of what is being lost.

The Global Reporting Wave

What is happening in 2026 is not a series of isolated national decisions. It is a coordinated global standard being implemented across dozens of jurisdictions within the same 24-month window, designed specifically to give tax authorities the same visibility over crypto activity they already have over bank accounts.

The OECD’s Crypto Asset Reporting Framework (CARF) is the architecture behind this shift. Developed by the Organisation for Economic Co-operation and Development and adopted at G20 level, CARF requires crypto asset service providers such as exchanges, brokers, and wallet providers, to collect detailed user and transaction data and report it automatically to their home country’s tax authority, which then shares it with the tax authorities of each user’s country of residence. As of March 2026, 76 Global Forum members have committed to CARF implementation.

CARF does not target individual players. It targets the exchanges and wallet providers those players use to acquire crypto. The effect on player privacy is the same

EU DAC8 – January 2026

The European Union’s implementation of CARF, the Eighth Directive on Administrative Cooperation, known as DAC8, took effect on 1 January 2026. All crypto service providers operating in the EU, or serving EU residents from anywhere in the world, are required to collect detailed user and transaction data from 1 January 2026 and report it to national tax authorities. The compliance deadline for exchanges is 1 July 2026. The first automatic exchange of information between EU member states covering all 2026 transactions will take place by 30 September 2027.

⃝ DAC8

DAC8

Reporting begins

Jan 1, 2026

First automatic exchange

Sep 30, 2027

Member states

27 EU Countries

Crypto activity becomes visible across the EU tax reporting network.

The scope is broader than most players realize. DAC8 applies not only to EU exchanges but to any global platform serving EU residents. A Curaçao licensed exchange with European users must comply. It covers full user identity, all transaction values, portfolio holdings, and associated wallet addresses. The European Commission was explicit. It is designed to give EU tax authorities “visibility over crypto holdings and transfers similar to what they currently have for traditional bank accounts.”

Ireland, whose Revenue Commissioners implement DAC8 directly, now receives transaction data on Irish crypto users from every reporting exchange. An Irish player buying USDT on Coinbase and depositing it at an offshore casino creates a traceable record at the exchange level that the Revenue Commissioners will receive automatically in 2027.

India – NTAA 2025 and VDA Reporting

India’s National Tax Administration Act 2025, effective from 2026, introduced Virtual Digital Asset reporting requirements that bring crypto fully into India’s tax reporting infrastructure. Domestic exchanges including CoinDCX, CoinSwitch, and ZebPay are required to file transaction records linked to users’ National Identification Numbers (NIN) and Tax Identification Numbers (TIN). The 1% Tax Deducted at Source on crypto transactions already creates a real-time audit trail for every purchase.

India’s VDA framework is designed to make under-reporting of crypto gains structurally difficult rather than merely illegal

Nigeria – ISA 2025

Nigeria’s Investment and Securities Act 2025, signed in March 2025, brought crypto under SEC oversight and mandated the linking of all exchange transactions to NIN or TIN. What had previously been a largely invisible P2P market is progressively being brought within a formal reporting structure. The EFCC’s September 2024 freezing of accounts belonging to large scale USDT traders, specifically citing exchange rate manipulation concerns, demonstrated that Nigerian financial crime authorities have both the appetite and the legal tools to pursue crypto activity that attracts attention.

Kenya – Finance Bill 2026

Kenya’s Finance Bill 2026, published in late May 2026 and currently under parliamentary scrutiny, proposes requiring all Virtual Asset Service Providers operating in or serving Kenyan users to file annual information returns with the Kenya Revenue Authority disclosing user identities, transaction histories, and wallet activity. The bill explicitly provides for international exchange of this data under CARF aligned frameworks. A KES 1 million penalty applies for failure to file. The proposed legislation arrives just months after the VASP Act 2025 created Kenya’s first dedicated crypto licensing framework. Combined, these frameworks close the gap between crypto’s practical operation in Kenya and the formal tax system’s visibility over it.

Major crypto gambling markets are moving into coordinated reporting systems.

Major crypto gambling markets are moving into coordinated reporting systems.

The United States – Two Systems Running in Parallel

The US approach is more layered than any other jurisdiction covered here, and understanding it requires separating two distinct but complementary systems: Form 1099-DA, which is already live, and CARF, which closes the gap 1099-DA leaves open.

Form 1099-DA

Form 1099-DA took effect for the 2025 tax year, requiring all US based custodial crypto brokers like Coinbase, Kraken, Gemini, and every other centralised exchange operating in the US, to report digital asset sales, exchanges, and transfers directly to the IRS. Full cost basis reporting (the acquisition value and date of each asset, not just the proceeds) becomes mandatory for 2026 transactions, reported to the IRS in early 2027. There is no minimum threshold. Even a $1 transaction is reportable. Transfer reports reveal which external wallet addresses you control. A US player who buys USDT on Coinbase and transfers it to a personal wallet has already generated a reportable record under 1099-DA.

The foreign exchange loophole remained open.

Until CARF implementation, US taxpayers using offshore exchanges could often acquire crypto without generating a 1099-DA report to the IRS.

CARF Closes the Foreign Exchange Gap from 2027

CARF is where the gap closes. Unlike 1099-DA which only requires US exchange to report to the IRS, CARF is a cross border automatic exchange. Foreign exchanges serving US persons report their activity to their own country’s tax authority, which then forwards it to the IRS. Simultaneously, the IRS sends data on foreign persons using US exchanges to their home country authorities.

In practical terms, if a US player buys USDT on a foreign exchange and deposits it at an offshore casino, that activity currently leaves no domestic trail. From 2027, that foreign exchange is required to report it and the IRS will receive it automatically, cross-referenced against the player’s domestic tax filings.

The first CARF data exchanges involving US taxpayers are expected in 2027, with full cost basis reporting from foreign exchanges aligning in subsequent years. DraftKings rolling out Bitcoin deposits across Illinois, Kentucky, New Hampshire, and Vermont from late January 2026 brought crypto gambling explicitly within regulated, reporting financial infrastructure for the first time in a major US market, a signal of where the rest of the landscape is heading.

The combination of 1099-DA and CARF creates near complete coverage. 1099-DA closes the domestic gap, CARF closes the foreign exchange gap. By 2028, the window in which a US player can acquire crypto and gamble offshore without that activity being visible to the IRS will be extremely narrow.

⃝ Two Systems. One Outcome.

Domestic reporting

Form 1099-DA

Tracks activity on US-based exchanges and custodial platforms.

International reporting

CARF

Enables automatic cross-border exchange of crypto transaction data.

Combined effect

Near-total visibility

Domestic exchange records and international exchange records increasingly connect to the same taxpayer profile.

The Exchange Is the Chokepoint

Understanding why this matters for casino players requires understanding where the actual privacy gap is being closed.

The offshore casino itself is not the target. A no-KYC casino licensed in Curaçao is under no obligation to report your activity to your domestic tax authority, and that has not changed. The casino does not know your name. It knows your wallet address.

The exchange does know your name. It also knows your wallet address because you withdrew from your exchange account to that wallet. That link, combined with the on-chain record of the subsequent transfer to a casino deposit address, is sufficient for a tax authority to reconstruct the transaction.

The exchange is becoming the key reporting point in the crypto gambling flow.

The exchange is becoming the key reporting point in the crypto gambling flow.

This is what CARF and DAC8 are designed to exploit. The on-chain record is public and permanent. The exchange record connects the wallet to an identity. The reporting obligation moves that connection from the exchange’s private database into the tax authority’s systems automatically. The player does not need to file anything. The exchange files on their behalf.

For the majority of recreational crypto casino players who buy USDT on Coinbase or Binance, transfer it to a personal wallet, and deposit it at an offshore platform, the practical privacy protection of their gambling activity is now significantly lower than it was two years ago. They may not know this. The reporting is not visible to them. It happens at the exchange level, in the background, on a schedule they never see.

As one crypto tax platform summarised the shift: “Your crypto exchange will automatically report your data from 01/01/2026 onward to the tax authorities. The Wild West era in crypto is over.”

What the Casinos Are Doing

Offshore casino operators are not passive observers of this shift. The response across the industry has split clearly into two camps.

Industry Split

| Compliance Path | Privacy Path |

| MGA-focused platforms | Curaçao / Anjouan-focused platforms |

| More KYC requirements | Less KYC friction |

| Better banking access | Stronger privacy positioning |

| Regulatory growth strategy | Privacy retention strategy |

The compliance accelerators: Primarily platforms with MGA (Malta Gaming Authority) licenses or those seeking regulated market access in newly licensing jurisdictions like Ireland and Kenya are voluntarily tightening their own KYC frameworks ahead of regulatory requirements. The logic is commercial: MGA licensed status signals legitimacy to the payment processors, banking partners, and institutional advertisers that are increasingly necessary for scale. Accepting stricter KYC now is the price of accessing those relationships.

The privacy defenders: Primarily Curaçao and Anjouanlicensed platforms are doubling down on no-KYC as a product differentiator precisely because the exchange level reporting squeeze is intensifying demand from players who understand what is happening. These platforms are not becoming more private in any absolute sense, but they are maintaining the final layer of casino level anonymity while it still exists.

It is worth understanding what a Curaçao licence actually meant historically versus what it means now, because the distinction matters for players choosing platforms. Under the old system, four private companies held master licences from the Curaçao government. Those four companies could sell sub-licences to anyone wanting to run a casino, acting as unaccountable middlemen with almost no incentive to vet who they approved. The Curaçao government had virtually no direct visibility over the thousands of casinos operating under these sub-licences. The barrier to entry was low, the scrutiny was minimal, and “Curaçao licensed” became shorthand for the loosest available regulatory fig leaf in the industry.

Curaçao’s Big Reset

Curaçao’s Big Reset

Before 2024

Master Licence → Sub-Licences

Private intermediaries sold sub-licences with limited direct government oversight.

After 2024

Casino → Curaçao Gaming Authority

Operators apply directly to the CGA and remain accountable to a single regulator.

The old master-license system was abolished in December 2024.

Curaçao’s LOK (National Ordinance on Games of Chance), enacted on 24 December 2024, abolished that system entirely. The four master license holders no longer exist in that capacity. Every casino must now apply directly to the newly established Curaçao Gaming Authority (CGA) for its own licence, meet the CGA’s standards directly, and remain accountable to the CGA as the sole regulator. A casino holding a new CGA licence is operating under a meaningfully stricter framework than one that grandfathered in under the old sub-license model, a distinction worth checking when evaluating platforms.

The split is not permanent. Regulatory pressure tends to converge. Platforms that have chosen the compliance path will benefit from mainstream legitimacy. Platforms that have chosen the privacy path will face progressively greater difficulty accessing payment infrastructure as CARF implementation tightens exchange relationships globally.

What Players Can Still Do to Maintain Privacy

Privacy in crypto gambling is eroding, not gone. There are genuine tools that remain effective, though each has trade-offs.

Monero (XMR) is the most structurally private option available. Unlike Bitcoin or Ethereum, which record all transactions on a fully public ledger, Monero uses ring signatures, stealth addresses, and confidential transactions to hide the sender, receiver, and amount of every transaction. There is no public blockchain trail to follow. The acquisition problem remains as buying Monero with fiat currency requires a KYC exchange in most jurisdictions, but the on-chain footprint of subsequent activity is genuinely opaque in a way that Bitcoin fundamentally is not. Monero is accepted at a growing number of offshore casinos, though the selection remains narrower than BTC or USDT.

Bitcoin Lightning Network payments do not leave individual transaction records on the main Bitcoin blockchain. Lightning payments are settled off-chain and only the channel opening and closing transactions appear on-chain. For a player using a Lightning enabled casino, the individual deposit and withdrawal are not directly visible to blockchain analytics tools. This is a meaningful privacy improvement over mainchain Bitcoin, though acquiring Lightning ready Bitcoin still requires exchange interaction in most cases.

Non-reporting jurisdictions: Countries where crypto exchange regulation has not yet implemented CARF remain outside the automatic reporting network. This is a shrinking category. As of March 2026, 76 Global Forum members have committed to CARF. By 2027 or 2028, the number of jurisdictions outside the framework where players can buy crypto without generating a reportable record will be very small.

DAC8’s smart contract gap: One acknowledged limitation of DAC8 is that smart contracts without intermediaries are explicitly excluded from its reporting scope. Fully decentralised crypto gambling protocols, where a player interacts with a smart contract directly without an intermediary, fall outside the framework. This is a real gap, though the accessible game quality and player experience on fully decentralised platforms remains well behind centralised offshore casinos in 2026.

Monero Remains the Privacy Leader

Ring signatures, stealth addresses, and confidential transactions hide the sender, receiver, and amount of each transaction in ways that Bitcoin fundamentally does not.

None of these tools restore the three layer anonymity that existed before 2022. They reduce the trail. For most recreational players making modest deposits, the realistic enforcement risk from residual visibility remains low. For high volume players with significant winnings, the risk calculus is meaningfully different.

Why This Is Actually Good for the Industry

The case for the end of anonymous gambling is not just a regulatory inevitability, it is, in several important respects, good for the long-term health of the industry.

Crypto Gambling Is Now Mainstream

Global iGaming share

17%

Estimated share of global iGaming betting volume.

Stake annual GGR

$4.7B

Reported gross gaming revenue scale.

Monthly wagering volume

$10B

Estimated monthly wagering activity.

The crypto casino market has grown from virtually nothing to representing nearly 17% of all global iGaming bets in five years. Stake Casino, the world’s largest crypto casino, generates $4.7 billion in gross gaming revenue and processes an estimated $10 billion in monthly wagers. These are not underground numbers. This is mainstream scale.

That mainstream scale brings mainstream scrutiny. Regulatory frameworks that improve player protection, push scam platforms out of the market, and create enforceable dispute resolution mechanisms benefit legitimate players more than they harm them. The era of anonymous gambling was also the era of rampant exit scams, withdrawal traps, and fake provably fair systems because the same anonymity that protected players also protected bad operators.

DraftKings accepting Bitcoin. Ireland issuing remote gambling licences. Kenya formalising its gambling framework. These are developments that increase player protection and market legitimacy simultaneously. They come at a privacy cost. Whether that trade-off is worthwhile depends on what you value, but the argument that regulation only harms players and protects nobody is harder to sustain at this stage of the market’s development.

The Honest Picture in 2026

Tax authorities across 76 committed jurisdictions will receive data on crypto transactions made from 1 January 2026 onward. By September 2027, that data will be in the hands of tax authorities across all 27 EU member states and dozens of other jurisdictions. The first wave of letters from revenue authorities to crypto users who failed to declare gains from gambling related disposals will follow shortly after.

Most recreational players will not be affected. Small scale activity, losses that generate no taxable gain, and activity within annual exemption thresholds will pass without consequence. The players who face genuine exposure are those who made significant undeclared gains on crypto that appreciated between purchase and casino deposit, a scenario that the 2021–2024 bull market created in abundance.

The offshore casino still does not know your name. But your exchange does, your tax authority will, and the on-chain record linking your wallet to your gambling activity is permanent. In 2026, that chain is shorter and more legible than most players realise.

The anonymous gambling era was not killed by one government or one regulation. It was closed by a spreadsheet, filed by your exchange, received by your tax authority, effective from 1 January 2026.

This article is for informational purposes only and does not constitute legal or tax advice. Consult a qualified professional in your jurisdiction for guidance on your specific situation.

The post The End of Anonymous Gambling: How 2026’s Global Privacy Crackdown Is Reshaping Crypto Casinos appeared first on BitcoinChaser.

추천 콘텐츠

Is retail coming back to crypto? What the search data says

Drift Protocol Breach Triggers Up to $285 Million Losses

Phemex Publishes April 2026 Proof of Reserves, Reporting 131% Total Reserve Ratio

인기 뉴스

더보기