Taiwan Semi Price Prediction and Forecast 2026–2030: How Much Upside Ahead?

The post Taiwan Semi Price Prediction and Forecast 2026–2030: How Much Upside Ahead? appeared first on 24/7 Wall St..

Taiwan Semiconductor Manufacturing (NYSE:TSM) is the most important company in the AI supply chain that nobody can replace. CEO C.C. Wei told investors that “global chip supply will not meet AI-fueled demand for years” and reiterated over 30% full-year revenue growth for 2026.

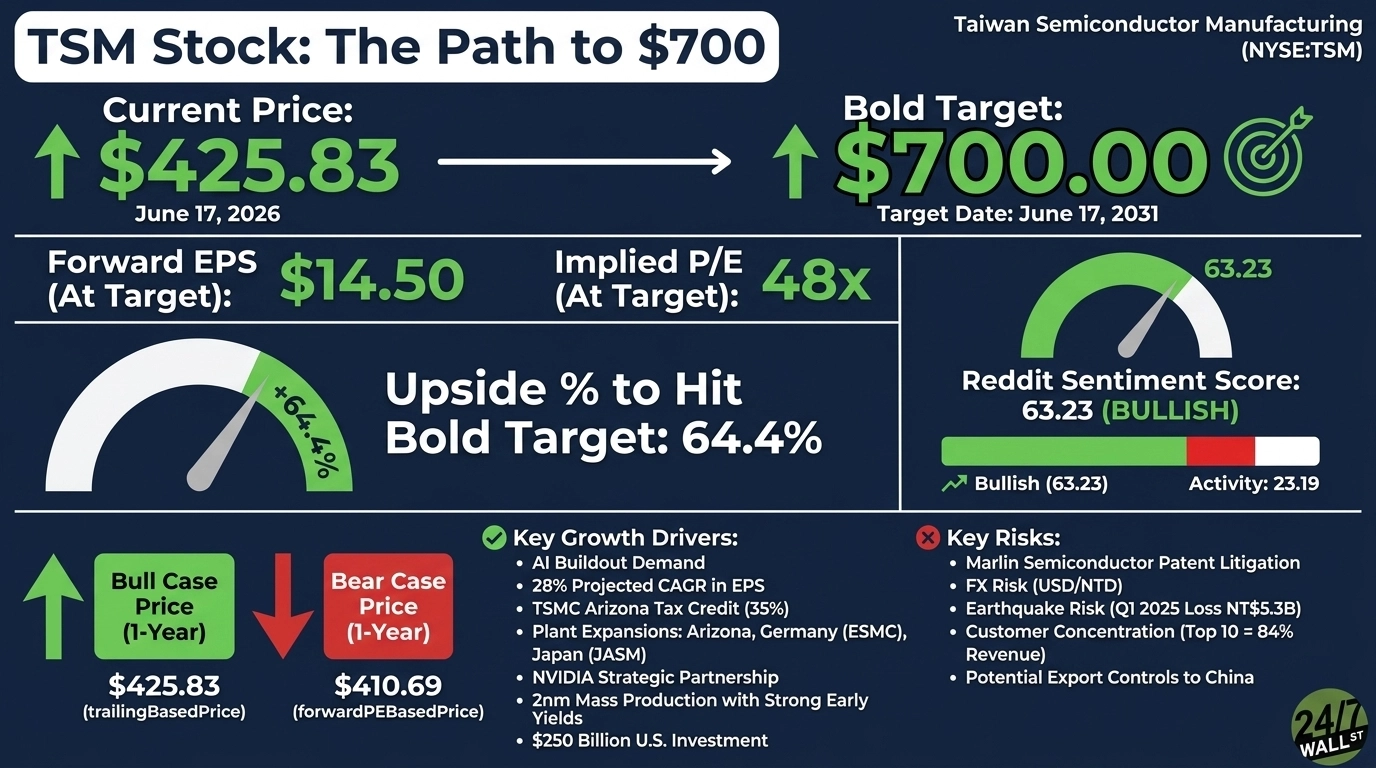

Shares are up 40.83% YTD and 99.57% over the past year. The question I want to answer: can TSM hit $700 by 2030?

I think the path exists. Let me show you the math.

What’s Holding TSM Back Right Now

Even with the 1-year ramp, TSM has stalled near record territory. Shares are down 0.26% over the past week and gave back 3.42% on June 16 on profit-taking and Samsung competition chatter.

A patent dispute involving Marlin Semiconductor and Longitude Licensing is now in front of the U.S. International Trade Commission. Taiwan is also considering stricter export controls on advanced AI chips to China, which could pressure customer access.

Layer on a beta of 1.25 and a stock trading just 4% below its 52-week high of $449.33, and you have a name where every geopolitical headline gets weaponized into a 3% red day. That’s the setup.

The Consensus Is Bullish, But Here’s What It’s Missing

Wall Street’s consensus target sits at $467.84, with 5 strong buys, 12 buys, 2 holds, and zero sells. Our base case lands at $496.35, a 16.56% one-year upside with 90% confidence. The optimistic case stretches to $577.03.

My push-back on the sell side: analysts are anchoring on near-term capacity and margin dilution from Arizona, but 89% bullish sentiment with 58.4% quarterly earnings growth is not consistent with a $467 target. Bernstein’s 28% compound EPS growth projection through 2028 implies materially higher fair value than the consensus target.

The Path to $700 Per Share

Reaching $700 from today’s price of $425.83 would require a gain of 64.4%.

24/7 Wall St.

24/7 Wall St.

With forward EPS of $14.5, a $700 price implies a forward P/E of 48x. Our base case of $496.35 already implies 35x, so the bold target needs roughly 13x of additional multiple expansion. Stretched, but not crazy.

The compression story works if EPS keeps compounding. 2025 full-year EPS hit $10.65, up 76.3% from 2024’s $6.04. Q1 2026 EPS came in at $3.49, beating estimates by 8.39%.

Three catalysts I’d anchor on: the NVIDIA strategic partnership to integrate AI into TSMC’s fabs, 2nm mass production with strong early yields, and a $250 billion U.S. investment that defuses geopolitical discount. Wei also dismissed Samsung’s catch-up goal as a “pipe dream.”

The main risk: a Taiwan Strait escalation or aggressive U.S. export curbs would compress the multiple before EPS can grow into it.

Where TSM Trades Today vs Its Earnings Power

At the current price, TSM trades around 29x forward EPS of $14.5, with a trailing P/E of 38. That’s reasonable for a business growing earnings 58% year over year. Shares sit between a 52-week low of $204.32 and a high of $449.33, and the 10-year return of 2,019.15% shows what compounding inside the AI tailwind actually looks like.

Is $700 Realistic? Here’s My Take

$700 by 2030 demands a 64.4% gain from here. Realistic, with caveats.

Three things need to go right: EPS has to keep compounding above 20% annually through the 2nm and A13 ramp, the NVIDIA partnership has to translate into measurable yield and capacity wins, and Taiwan’s geopolitical risk premium needs to stay contained.

A serious China-Taiwan flare-up or a forced technology transfer mandate would derail the entire thesis. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Taiwan Semiconductor Manufacturing could reach $700 in 2030.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Taiwan Semiconductor Manufacturing didn’t make the cut. Grab the names FREE today.

The post Taiwan Semi Price Prediction and Forecast 2026–2030: How Much Upside Ahead? appeared first on 24/7 Wall St..

추천 콘텐츠

Best Altcoins to Buy: 3 Clever Projects That Can Lead the Next Crypto Wave

UK FCA May Exempt Crypto Firms from Key TradFi Rules — What’s at Stake?

Tokenization Revolution: IMF Declares Digital Assets are Reshaping Regulated Finance