Strategy’s STRC Preferred Stock Hits Record Low Below Par, Pausing Key Bitcoin Funding Channel

- Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock (STRC) closed at a record low of $89, 11% below its $100 par value.

- The discount has paused the company’s at-the-market issuance program, a primary channel for raising capital to acquire more bitcoin.

- This follows Strategy’s first-ever BTC sale of 32 coins for ~$2.5 million in late May to cover STRC dividends.

- Bitcoin and ether spot ETFs saw combined outflows of $111 million amid fading rate-cut expectations.

Strategy’s ambitious bitcoin treasury strategy faced fresh headwinds on Wednesday as its flagship funding instrument, the STRC preferred stock, traded to a record low, temporarily constricting one of the company’s key levers for accumulating more BTC.

The Variable Rate Series A Perpetual Stretch Preferred Stock (STRC), launched in July 2025 and designed to trade near $100 par while paying a variable dividend (currently yielding around 12.9% effective), closed at $89, according to market data. This marks the lowest level on record and an 11% discount, prompting Strategy to pause new share sales via its at-the-market program.

When trading above par, Strategy issues additional STRC shares and deploys the proceeds into bitcoin purchases, a mechanism that has significantly bolstered its holdings—now totaling approximately 846,842 BTC, or roughly 4% of Bitcoin’s eventual supply, making it the largest corporate holder. With the stock below par, that avenue is on hold, even as the firm continues smaller acquisitions funded by common stock sales.

The pressure on STRC comes shortly after Strategy disclosed its first bitcoin sale since beginning its accumulation in 2022: 32 BTC sold for about $2.5 million in late May specifically to fund distributions on the preferred stock. Chairman Michael Saylor has emphasized the company’s long-term commitment, noting a dedicated USD reserve of $1.1 billion for dividends and debt while continuing to add BTC.

Broader market context amplified the move. Spot bitcoin and ether ETFs recorded combined outflows of $111 million following the Federal Reserve’s hawkish signals under new Chair Kevin Warsh, with rate-cut hopes diminishing. Bitcoin hovered near $64,000, while Strategy’s common shares (MSTR) fell around 5%.

Analysts have pushed back against “death spiral” concerns, pointing to Strategy’s substantial bitcoin holdings providing ample coverage. However, the de-peg highlights risks in leveraging preferred equity for crypto treasury management, especially amid volatility and competing instruments like Strive’s SATA, which has traded near or above par.

In a governance or investor context, Saylor has positioned STRC as a cornerstone “digital credit” product offering yield backed by bitcoin exposure. The company maintains it has significant runway, with bitcoin holdings providing decades of potential dividend coverage under current parameters.

Bitcoin layer-2 developments, such as the recent Botanix shutdown citing insufficient demand for programmable BTC DeFi, further underscore a bear-market reality check for infrastructure plays, though Strategy’s approach remains firmly focused on direct holdings and yield products.

Traders and investors will watch whether STRC can stabilize or if further adjustments to the dividend rate are needed to restore confidence in the mechanism that has powered Strategy’s bitcoin-buying machine.

Disclaimer: This article is for informational purposes only and does not constitute advice of any kind. Readers should conduct their own research before making any decisions.

The post Strategy’s STRC Preferred Stock Hits Record Low Below Par, Pausing Key Bitcoin Funding Channel appeared first on Cryptopress.

You May Also Like

Dow Jones futures plunge as risk aversion increases after Trump’s comments

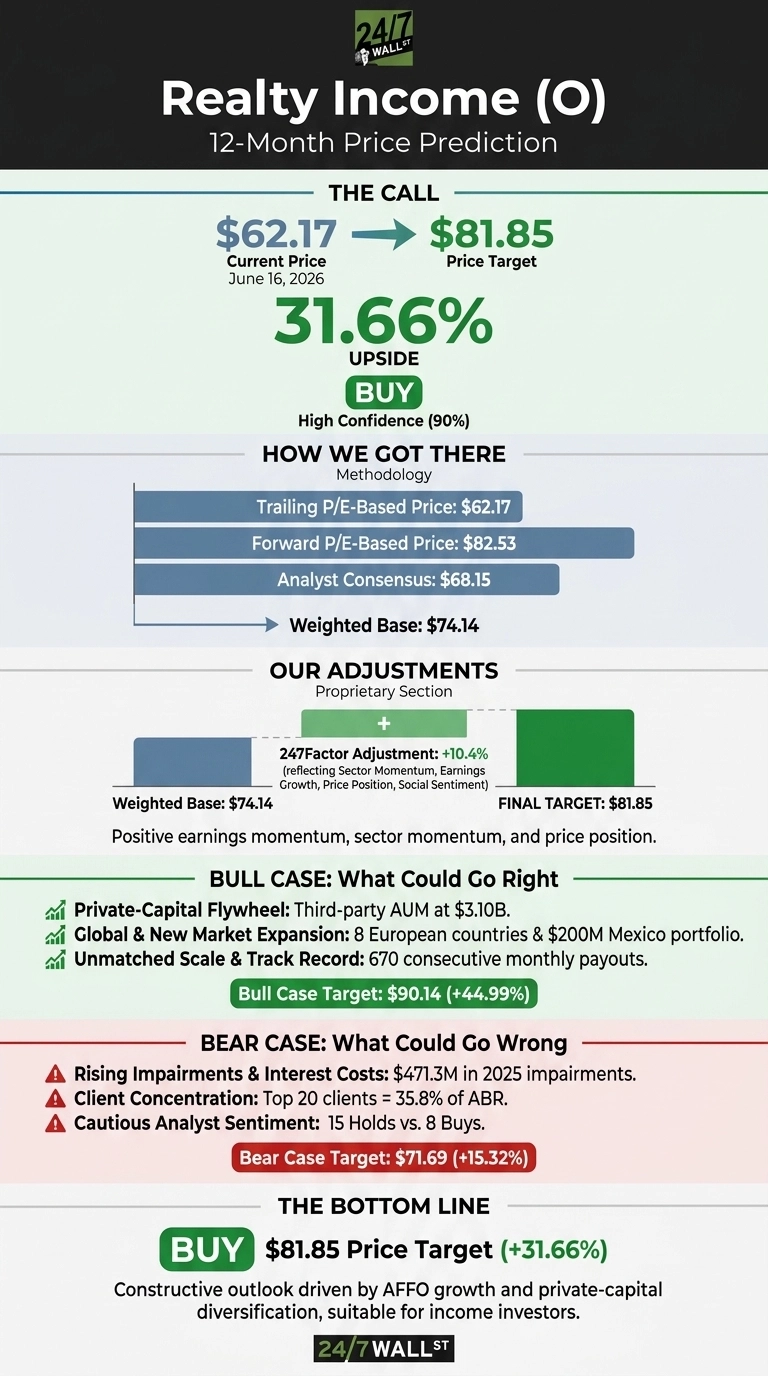

Our Highest Conviction Call on Realty Income Points to 30% Upside

Richard Harris Law Firm Partners with CCSD to Honor School Bus Drivers at Appreciation Event