FedEx Freight’s First Earnings Test: Can FDXF Prove the Spinoff Premium?

FedEx Freight is on the clock. The newly independent less-than-truckload (LTL) carrier started regular-way trading on the NYSE under the ticker FDXF on June 1, 2026, marking the formal split from its former parent, FedEx. The setup is classic spinoff material: a focused operating model, a fresh balance sheet, and a market eager to test whether the story deserves a higher multiple than it did inside the conglomerate. FedEx Freight press release

The first real check-in arrives on June 25, 2026, when FDXF will report its Q4 FY2026 results after the close and hold an earnings call at 4:00 p.m. CDT (5:00 p.m. ET). The call isn’t just a readout—it’s a referendum on the spinoff premium narrative. FedEx Freight press release

There are important moving pieces. Ahead of the separation, FedEx Freight paid a roughly $4.1 billion cash dividend to its former parent, financed by a $3.7 billion senior notes offering and a delayed-draw term loan, per its Form 8-K. That leaves investors to parse leverage, interest burden, and capital allocation priorities on day one. SEC Form 8-K (FedEx/FedEx Freight)

There’s also an ownership wrinkle: FedEx retained 19.9% of FDXF and says it intends to dispose of that stake within 24 months. The timing and method could weigh on the tape—or provide incremental liquidity and index eligibility, depending on execution. FedEx newsroom press release

Point Details First earnings test Q4 FY2026 release and call on June 25, 2026 at 4:00 p.m. CDT (5:00 p.m. ET); watch guidance tone and operating cadence. FedEx Freight press release Balance sheet after spin About $4.1B dividend to former parent, funded by $3.7B notes plus a term loan; interest coverage and deleveraging plan are pivotal. SEC Form 8-K Ownership overhang FedEx kept 19.9% with an intent to dispose within 24 months; potential overhang vs. float expansion dynamic. FedEx newsroom Spinoff premium drivers Density-focused network execution, disciplined yield management, steady service KPIs, credible capital allocation and governance. Top risks Freight-cycle volatility, pricing missteps, elevated leverage, labor and maintenance costs, and potential supply-demand imbalances.

Why this first print matters for a spinoff premium

Spinoffs often promise sharper focus, cleaner incentives, and better capital discipline. But the market only awards a “spinoff premium” when early evidence confirms that promise. For an LTL carrier, that means the quarterly script must connect a few dots: stable volumes, rational pricing, operational consistency, and a repeatable plan to pay down debt while investing in service quality.

If management pairs those fundamentals with transparent guidance and guardrails (what they will and won’t chase on price or volume), the stock can earn patience. If the call leans on one-time adjustments, opaque yield talk, or “wait-for-next-year” narratives, the premium can vanish as quickly as it appeared.

What to watch on June 25: metrics, language, and sequence

Core operating cadence

- Volume and mix: Tonnage per day and shipments per day directionally; commentary on weight per shipment and length of haul.

- Yield discipline: Revenue per hundredweight ex-fuel and the balance between account retention and price increases.

- Service reliability: On-time performance, claims ratio, and terminal throughput productivity—any quantitative or qualitative color helps.

Costs and efficiency

- Linehaul and purchased transportation trends; tractor and trailer utilization; dock labor efficiency and overtime control.

- Fuel surcharge mechanics and whether they’re offsetting underlying cost inflation.

- Maintenance cadence: parts availability, shop hours, and downtime reduction initiatives.

Profitability lens

- Operating ratio (with and without fuel) and the size of any one-time items.

- Incremental margins commentary: how pricing, volume, and mix feed through to contribution.

Balance sheet and cash

- Interest expense run-rate and sensitivity to rates.

- Capex priorities: tractors, trailers, terminals, tech, safety—plus replacement vs. growth split.

- Working capital: seasonality in receivables and any DSO movement.

Strategy and guidance

- Capital allocation sequence: deleveraging milestones versus opportunistic growth.

- Customer segmentation plans: national accounts vs. regional/SMB mix and contract renewal cadence.

- Full-year guideposts: not just revenue and margins, but the KPIs they’ll hold themselves to.

Pro tip: Track how management bridges “ex-fuel” yield and any service claims to the operating ratio. If the bridge is crisp and repeatable, you have a baseline for future quarters.

Remember, this is the first call as a standalone public company. It sets tone more than it sets precise ranges. Still, the date and time are locked: June 25 at 4:00 p.m. CDT (5:00 p.m. ET). FedEx Freight press release

Capital structure after the spin: dividend recap and runway

Spinoffs sometimes arrive levered because the unit pays a dividend to the parent before separation—a classic dividend recap. That’s the case here: approximately $4.1 billion was distributed to FedEx ahead of the effective time, funded by a $3.7 billion senior notes offering and borrowings under a delayed-draw term loan, according to FDXF’s Form 8-K. SEC Form 8-K

For investors, the questions aren’t just “how much debt?” but “what kind of debt, and how fast can it come down?” Watch for:

- Fixed vs. floating mix and maturities: refinancing risk and exposure to rate volatility.

- Interest coverage thresholds: management’s comfort zone and covenant headroom if applicable.

- Deleveraging plan: target net leverage trajectory and the balance between debt paydown and fleet/terminal investment.

- Liquidity stack: revolver availability, cash balance philosophy, and working-capital seasonality.

Dividend recaps can be an overhang if the company chases volume to “grow into” leverage. They can also be fine if operating discipline turns cash conversion efficiently. Expect close analyst scrutiny of interest-expense guidance and sensitivity analysis on rates.

Governance, incentives, and the 19.9% overhang

FedEx retained a 19.9% stake in FDXF at distribution and stated it intends to dispose of that interest within 24 months, potentially to repay debt or via distributions. FedEx newsroom That creates two simultaneous dynamics:

- Overhang risk: The market may discount the shares until the path and pace of disposition are clearer.

- Float and ownership quality: A well-executed secondary or distribution can broaden the shareholder base and improve index inclusion odds.

On governance, investors will want clarity on board composition, compensation levers tied to service and return metrics, and safeguards against short-termism. Spinoffs that tie pay to high-integrity KPIs (service reliability, safety, free cash flow after maintenance capex) tend to earn more trust than those reliant on adjusted earnings alone.

The LTL playbook that earns a premium

Build and protect density

LTL is a density game. The more shipments you consolidate efficiently across a network of terminals, the more you can sweat fixed assets and reduce empty miles. Premiums accrue to carriers that expand densest lanes, prune low-quality freight, and add terminals or dock doors where bottlenecks occur.

Price with discipline, not aggression

Yield management works when carriers hold the line on underpriced freight and negotiate based on service value rather than headline discounts. The best operators talk openly about walking away from business that doesn’t meet return thresholds and about customer cohorts where service justifies above-market renewals.

Operational reliability as a brand

On-time performance, low claims, visible tracking, and consistent pickup/delivery windows create stickiness. Those service KPIs can support mid-cycle pricing and help carriers avoid spikes of purchased transportation when volumes flex.

Invest where it compounds

- Fleet: tractors and trailers that improve uptime and fuel efficiency.

- Terminals: dock-door capacity and cross-dock design to cut touches and improve damage rates.

- Technology: shipment visibility, dynamic routing, dock scheduling, and data tools to steer yield decisions.

- People and safety: driver retention, training, and incident reduction.

How investors may frame FDXF against LTL comps

Public LTL peers typically trade on a blend of operating ratio credibility, through-cycle free cash flow, network density, and quality of management guidance. Without anchoring to specific peer multiples, you can still map the signals that distinguish “premium” from “discount” stories.

Signal Premium read Discount read Yield commentary Clear ex-fuel trends with mix and service context Headline price talk without bridge to margins Volume strategy Selective growth in densest lanes; prune low-return freight Chasing volume to cover fixed costs Service KPIs Specific on-time and claims improvements Vague references to “customer experience” Capex plan Maintenance first, targeted growth capex with ROI guardrails Broad “growth” spend without thresholds Leverage path Time-bound delever targets and interest sensitivity “We’ll manage it” without milestones Guidance culture Conservative, beat-and-raise bias Optimistic guides that later require resets

Scenarios for year one—and a buyer’s checklist

Three directional scenarios

- Bull setup: Volumes stabilize, yield holds ex-fuel, operating discipline shows through, and management outlines a credible deleveraging path alongside targeted reinvestment. The stock earns patience and potentially a premium narrative.

- Base case: Mixed volumes with disciplined pricing; service metrics trend better but not linearly; deleveraging proceeds, albeit slowly, with clear milestones.

- Bear path: Competitive pricing erodes yield; purchased transportation or maintenance costs rise; leverage optics worsen and the ownership overhang pressures the multiple.

A practical checklist for the call

- Did management quantify ex-fuel yield and tie it to service improvements?

- Are volume comments aligned with network density goals rather than raw market share?

- Is there a bridge from reported OR to underlying run-rate excluding one-times?

- What is the capex split between maintenance and growth, and what ROIC hurdles apply?

- How explicit is the deleveraging plan (targets, timing, interest sensitivity)?

- What is the stated policy on low-return freight and price discipline?

- How will the company handle the 19.9% stake disposition dynamics from the former parent?

Avoidable pitfalls and the real risks

- Reading too much into one quarter: Early spinoff prints are noisy. Focus on run-rate signals and policy choices.

- Ignoring the cost of capital: A dividend recap raises the bar for project returns. Demand clarity on interest coverage and hurdle rates.

- Underestimating cycle risk: LTL demand ties to industrial activity and retail restocking; shipment counts can whipsaw.

- Assuming pricing immunity: Even disciplined carriers face pressure if peers discount to chase volumes.

- Forgetting labor and maintenance inflation: Wage steps, parts, and shop time can compress margins if not offset by yield or productivity.

- Overlooking ownership overhangs: Large secondary moves or distributions can affect supply/demand for shares in the short run.

- Relying on adjusted figures alone: Scrutinize adjustments and reconcile to cash; free cash flow after maintenance capex matters.

Valuation lenses: what matters beyond the multiple

Headline multiples will move, but the durability of any spinoff premium depends on the cash engine. Through-cycle, the market tends to reward LTL carriers that turn consistent operating discipline into high-conviction free cash flow. For FDXF, that chain likely runs through five links: service reliability, yield quality, density expansion, cost control, and debt reduction.

Listen for how management defines success and failure. The best roadmaps set explicit thresholds—service levels to be met before growth, ROI hurdles for dock-door additions, payback periods for fleet refreshes, and leverage gates before any discretionary shareholder returns are considered.

In short: a premium is earned by process, not promises.

FDXF’s context is specific. It’s a just-spun, NYSE-listed LTL operator, with a meaningful debt load from a pre-spin dividend, and a 19.9% owner preparing to exit over up to two years. Each of those inputs is known from company disclosures; what the market needs now is evidence on execution. FedEx Freight press release SEC Form 8-K FedEx newsroom

For investors, the posture is straightforward: take notes, build bridges from statements to cash, and revisit the thesis as the first few quarters either narrow or widen the execution gap.

Not financial advice. Public equities involve risk, including potential loss of principal. Do your own research.

If you want ongoing analysis of market structure and how logistics, payments, and digital-asset rails intersect, keep an eye on coverage at Crypto Daily.

Frequently Asked Questions

What is FDXF and where does it trade?

FDXF is the ticker for FedEx Freight, the less-than-truckload carrier that was spun off from FedEx. It began regular-way trading on the New York Stock Exchange on June 1, 2026. FedEx Freight press release

When is FedEx Freight’s first earnings call as a standalone company?

FDXF will report fourth-quarter fiscal 2026 results and host its earnings call on June 25, 2026 at 4:00 p.m. CDT (5:00 p.m. ET). FedEx Freight press release

What is a “spinoff premium,” and why does it matter for FDXF?

A spinoff premium is when the market assigns a higher valuation to a newly independent unit because it believes focused strategy, incentives, and capital allocation will improve performance. For FDXF, the first few quarters must signal durable pricing discipline, service reliability, and a credible path to deleveraging to justify such a premium.

How does the pre-spin dividend recap affect risk?

FDXF funded a roughly $4.1B cash dividend to its former parent using a $3.7B senior notes offering and a term loan, raising leverage and interest expense. The company’s ability to generate consistent cash, manage costs, and prioritize debt reduction will be central to its risk profile. SEC Form 8-K

What does FedEx’s 19.9% retained stake mean for shareholders?

FedEx retained 19.9% of FDXF at separation and intends to dispose of it within 24 months. The pending disposition can create a perceived overhang near term, but it may also expand float and broaden the shareholder base once executed. FedEx newsroom

Which metrics should retail investors focus on from the call?

Look for directional commentary on ex-fuel yield, tonnage and shipments per day, operating ratio and any one-time items, capex split and ROI thresholds, interest expense run-rate, and a time-bound deleveraging framework with clear milestones.

Is this investment advice?

No. This article is for informational purposes only and does not constitute financial advice. Public markets are volatile, and you should conduct your own research and consider your risk tolerance.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

You May Also Like

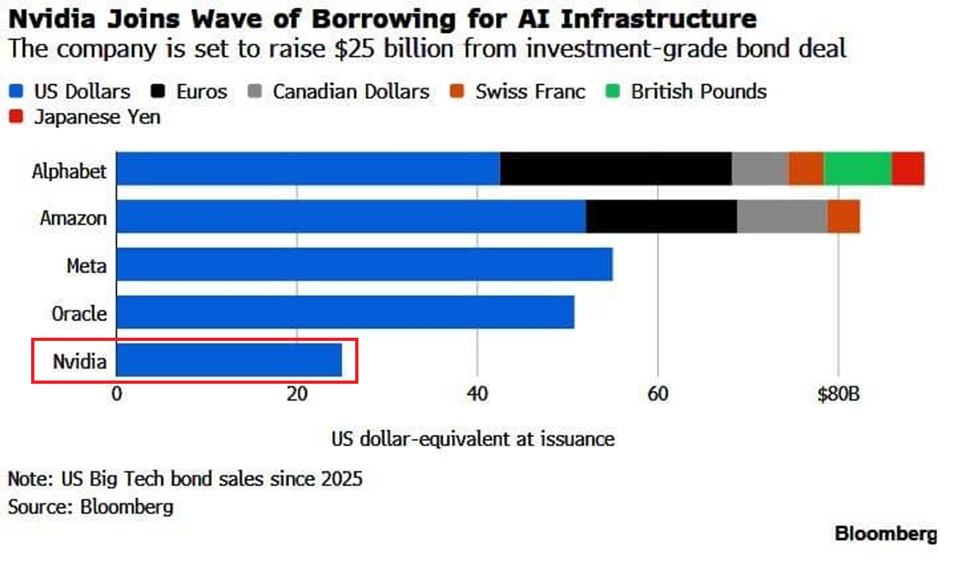

Nvidia Completes $25 Billion AI Debt Financing, Is NVDA Stock Ready for Next Rally?

Inside Trump's new weird obsession with the number 22

AI predicts XRP price for April 30, 2026