Down 50% In One Year, Can Planet Fitness Stock Stage a Comeback by 2028?

Key Takeaways:

- Member Growth Reset: Planet Fitness added over 700,000 net new members in Q1 2026, but missed internal expectations amid marketing and macro headwinds.

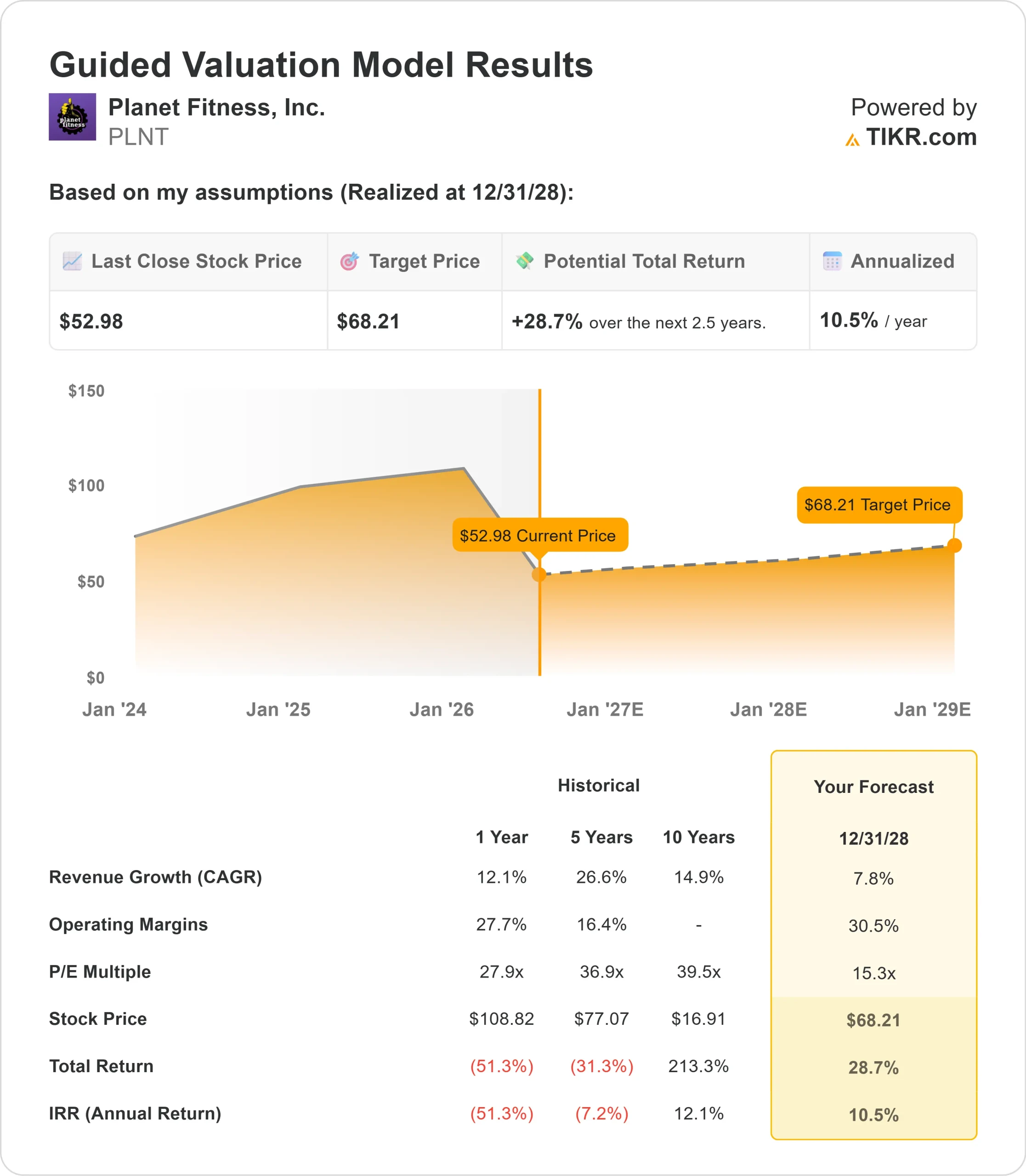

- Price Projection: Based on current assumptions, PLNT stock could reach $68.21 by December 2028.

- Potential Gains: That target implies a total return of 28.7% from the current price of $52.98.

- Annual Return: Investors could see roughly 10.5% annualized growth over the next 2.5 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Planet Fitness (PLNT) has had a painful stretch. The stock is down more than 50% from its 52-week high, dragged lower by slowing member growth, a guidance cut, and the decision to pause a planned price increase.

Q1 2026 results were a mixed bag as revenue came in at $337 million, up 22% year-over-year, and adjusted EBITDA rose 19.5% to $140 million.

On the surface, those are solid numbers. But net member additions of just over 700,000 fell short of the roughly one million the company added in Q1 last year — and management knows it.

CEO Colleen Keating was direct about the shortfall.

Marketing that resonated with fitness-minded consumers had drifted away from Planet Fitness’ core audience: the beginner.

The company has since paused its Black Card price increase and is reworking its creative strategy to win back that 70% of the population that still doesn’t belong to a gym.

See analysts’ full growth forecasts and estimates for PLNT stock (It’s free) >>>

What the Model Says for Planet Fitness Stock

We analyzed Planet Fitness through the lens of a business with a genuinely strong model that’s going through a self-inflicted reset.

The fundamentals haven’t broken down.

- Black Card penetration hit 67% in Q1, up 240 basis points year-over-year.

- Same-club sales grew 3.5%.

- The franchise system continues to expand, with 180 to 190 new club openings expected in 2026.

- Adjusted EBITDA margins remain healthy at 41.5%.

The problem is simpler than it looks. Planet Fitness shifted its marketing to attract more serious gym-goers, and it worked — too well.

It pulled in a narrower audience and left the fitness beginner, the brand’s bread and butter, underserved. A new creative agency has been hired. AI-enabled CRM tools and a dynamic content optimization engine are in development.

Management expects a new campaign to be in market before year-end, setting up a stronger Q1 2027.

The subscription model makes it hard to fully recover from a weak Q1 within the same year. A January join generates 12 months of revenue. A July join generates only six.

That math explains why the full-year guidance now calls for just 1% same-club sales growth and roughly 7% revenue growth.

Using a forecast of 7.8% annual revenue growth and 30.5% operating margins, with an exit P/E of 15.3x, our model projects Planet Fitness reaching $68.21 by December 2028. That’s a 28.7% total return, or 10.5% annualized.

The 15.3x P/E assumption sits well below PLNT’s one-year average of 27.9x and five-year average of 36.9x. The model assumes no re-rating, which makes it conservative. Any recovery in sentiment or membership momentum could meaningfully raise the multiple.

Our Valuation Assumptions

PLNT Stock Valuation Model (TIKR)

PLNT Stock Valuation Model (TIKR)

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PLNT stock:

1. Revenue Growth: 7.8%

Planet Fitness has grown revenues 12.1% over the past year and 14.9% annually over the past decade.

The 7.8% assumption reflects a period of slower growth as the company resets its marketing and rebuilds member momentum.

Management’s 2026 revenue growth guidance of approximately 7% is the anchor here.

2. Operating margins: 30.5%

Trailing EBIT margins are 29.9%, and the three-year average is 28.1%.

The 30.5% assumption reflects modest improvement as the franchise model’s natural operating leverage kicks in with revenue growth.

Equipment margins are already improving, hitting 31.3% in Q1.

3. Exit P/E Multiple: 15.3x

PLNT’s current NTM P/E is 16.3x — near multi-year lows.

The model assumes slight compression to 15.3x, acknowledging that the guidance reset and withdrawn three-year outlook have weighed on sentiment.

Historically, this stock has traded at a significant premium to this level.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Here’s how Planet Fitness stock could perform under different scenarios by December 2030:

- Low Case: With revenue growing at 6.5% and net income margins of 18.1%, investors could see a total return of 29.2% (5.8% annually).

- Mid Case: At 7.2% revenue growth and 18.6% net income margins, the total return climbs to 56.3% (10.3% annually).

- High Case: If revenue grows at 8% and margins reach 18.9%, total returns could hit 84% (14.4% annually).

PLNT Stock Valuation Model (TIKR)

PLNT Stock Valuation Model (TIKR)

See what analysts think about PLNT stock right now (Free with TIKR) >>>

The range comes down to one thing: whether the marketing reset works.

If Planet Fitness successfully reconnects with fitness beginners and reignites net member growth heading into 2027, the model’s upside case becomes highly achievable.

If member trends stay soft, the low case is the more likely outcome.

How Much Upside Does Planet Fitness Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Why QUICK Just Climbed 23.74% in 30 Minutes

Bitcoin ETFs Extend Six-Week Losing Streak Amid Franklin Templeton Filings

‘Bersatu kekal dalam PN sampai bila-bila’, kata Muhyiddin