Credo Just Tied Its CEO’s Pay to a $2.5 Billion Revenue Goal. Here’s Where the Stock Could Go

Key Stats for Credo Stock

- Current Price: $271.95

- Target Price (Mid): ~$720

- Street Target: ~$270

- Potential Total Return: ~165%

- Annualized Return: ~22% / year

- Earnings Reaction: +1.28% (June 1, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Credo Technology Group (CRDO) closed at $271.95 on June 30, up 10.69% in a single session. The move extended a strong June, a month in which the stock drew a wave of bullish Street action, including BofA lifting its target to around $340 and Stifel to around $350. The stock now sits near record territory, up roughly 85% since late February, though still below its intraday 52-week high of $308.67.

The rally is not the most revealing thing Credo did this month. On June 1, the same day it reported earnings, the board handed CEO Bill Brennan an equity award that pays out only if the company roughly doubles in size. Bulls read that as conviction. Bears read it as a board anchoring rewards to a valuation that already assumes years of flawless growth. The question the market cannot yet answer is whether the first target baked into that award is a stretch goal or a schedule. The answer decides whether the mid-$200s is a ceiling or a step.

A Pay Package That Only Works If Revenue Doubles

Alongside earnings, Credo disclosed a one-time equity grant to Brennan of up to 1,437,000 ordinary shares, structured as PSUs (performance-based restricted stock units, which convert to shares only if preset targets are hit). The award is 100% performance-based. It splits into six equal tranches of 239,500 shares and runs through June 30, 2031, per the company’s 8-K filing.

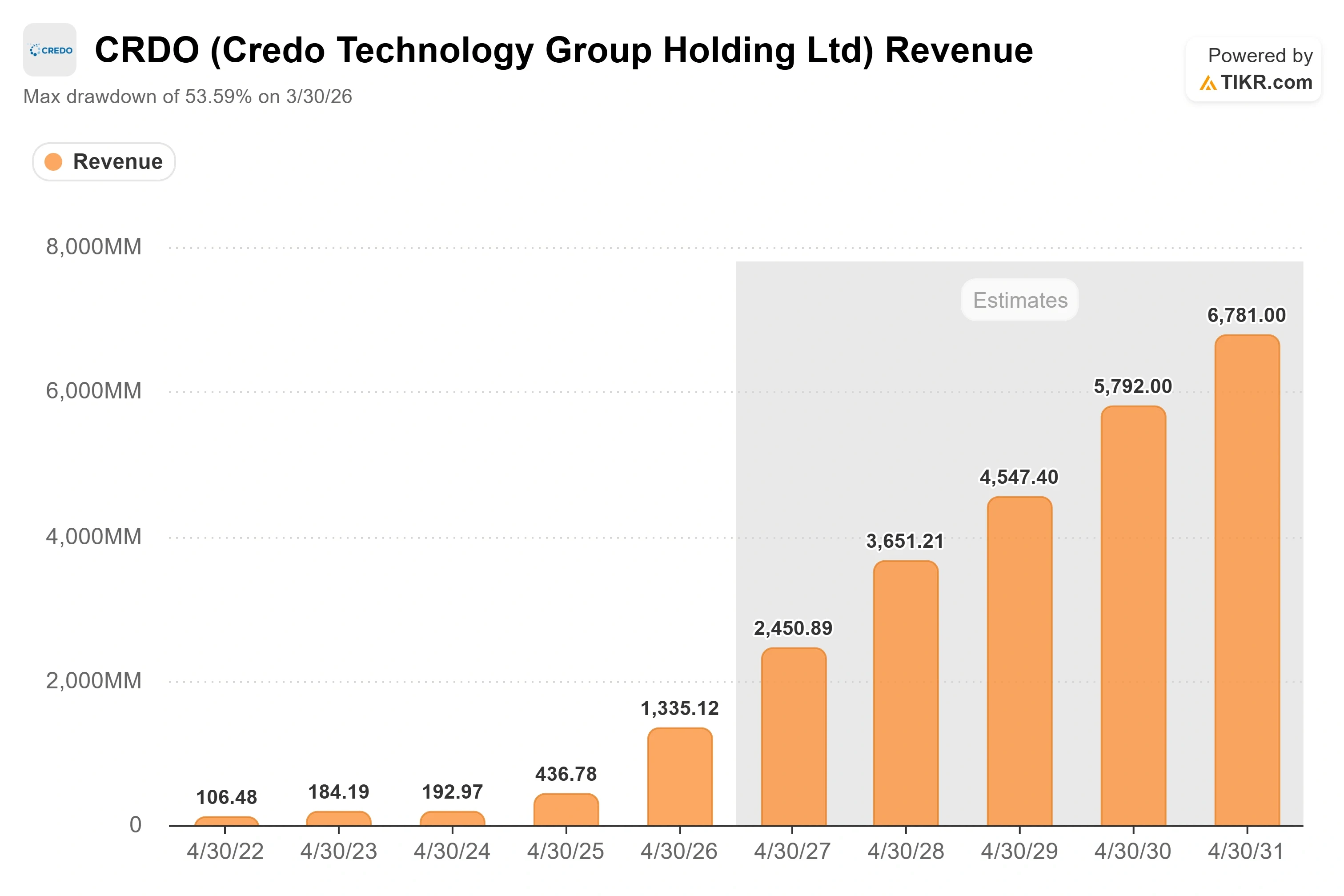

The hurdles are the story. The tranches unlock against revenue goals stepping from $2.5 billion up to $7.5 billion, paired with stock-price hurdles from $244.70 to $489.40. The first tranche requires $2.5 billion in revenue and a $244.70 share price. Credo just reported around $1.34 billion for fiscal 2026, so tranche one alone asks the CEO to nearly double the company. The top tranche asks for more than five times today’s revenue.

That structure is worth reading carefully. The lowest hurdle sits right where consensus already expects the business to be within a year, so the board is not reaching for a fantasy on tranche one. The $244.70 price hurdle has already been cleared, with the stock at $271.95. The revenue side has not, and that is where the debate lives.

Credo Revenue (TIKR)

Credo Revenue (TIKR)

See historical and forward estimates for Credo stock (It’s free!) >>>

Why Management Thinks It Can Get There

The $2.5 billion revenue hurdle is not pulled from thin air. Consensus already models Credo crossing it. TIKR data shows analysts expect fiscal 2027 revenue of around $2.45 billion, up around 84% year over year, which lands the company on the doorstep of tranche one within a year. Management’s own guidance points the same way, calling for more than 80% revenue growth in fiscal 2027, with fiscal Q1 guided to $465 million to $475 million.

The engine behind that number has two parts. The first is active electrical cables (AECs), short copper cables with built-in signal processors that link GPUs to switches inside AI racks. At the Bank of America 2026 Global Technology Conference on June 4, Brennan was asked when the AEC demand peaks. His answer was blunt: “I don’t see the peak.” He framed reliability as the company’s “North Star,” describing AECs as “1,000x more reliable than laser-based optics” for the no-redundancy links between GPUs and the first switch, where a single failure can stall an entire cluster. That reliability pitch is why AECs keep winning sockets even as the industry adds optics.

The second part is optics, and this is the fastest grower. Brennan said three optical lines, optical DSPs, silicon photonics chips, and ZeroFlap Optics will each cross $100 million and together top $600 million in fiscal 2027. Credo closed its around $750 million acquisition of DustPhotonics on May 28, bringing silicon photonics (chips that move data using light) in-house. CFO Dan Fleming underlined the model’s shape at the same conference, guiding operating expenses to grow around 50% while revenue grows more than 80%, because “there’s continuing leverage in the model.” Revenue outrunning costs is how a $2.5 billion target turns into profit, not just scale.

The Valuation Everyone Is Arguing About

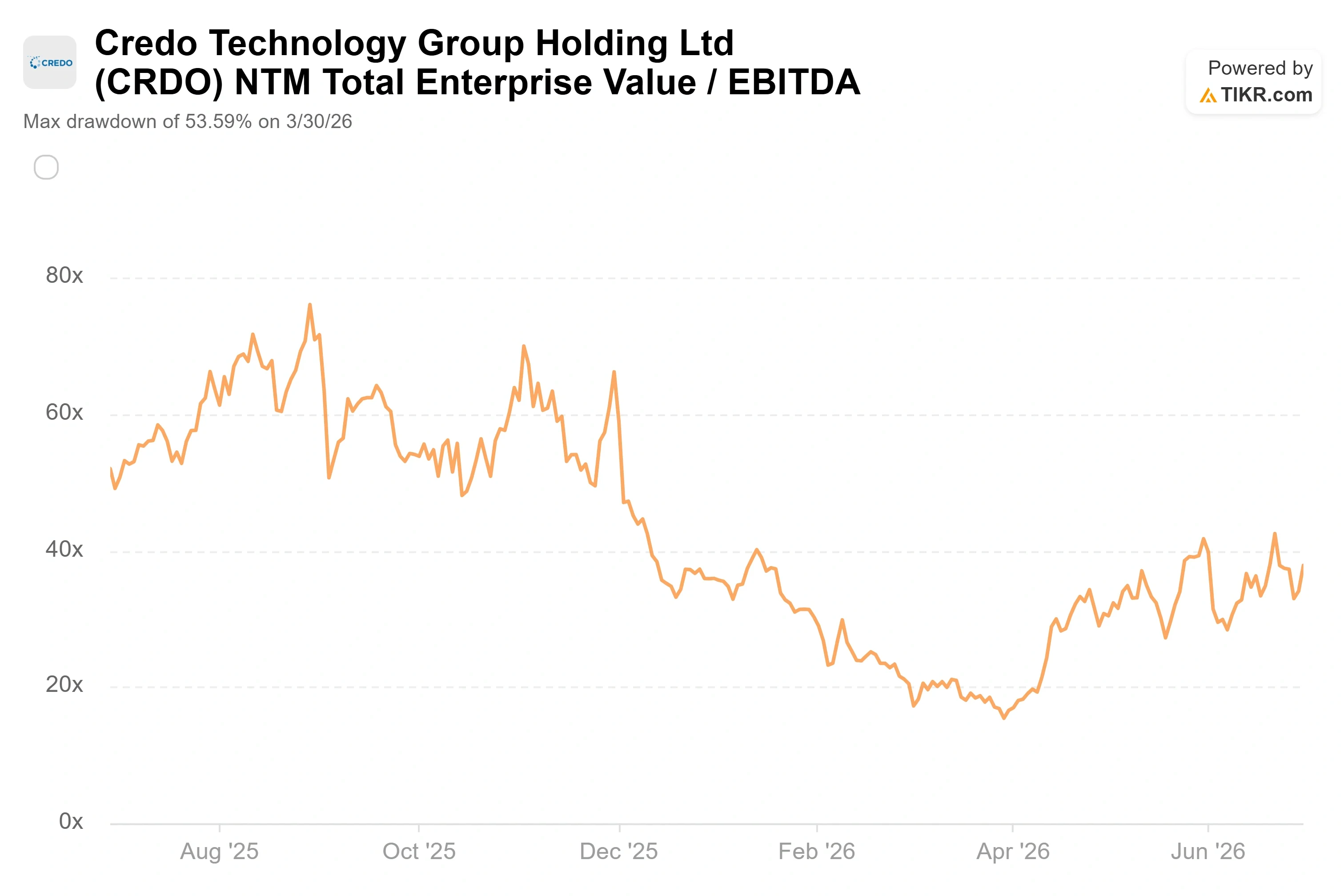

Credo’s results are not the debate. Fiscal 2026 revenue tripled to around $1.34 billion, non-GAAP net income rose more than five times to around $662 million, and the company holds a net cash balance sheet. The debate is price. Credo trades at an NTM (next twelve months) EV/EBITDA of around 38x and around 20x forward revenue.

Against peers, that is a clear premium on one measure and a modest step up on another. The semiconductor peer group mean sits near 35x forward EV/EBITDA, so Credo’s roughly 38x is only slightly above the group. But Marvell, its closest connectivity rival, trades near 52x on the same measure, while NVIDIA sits near 16x. On forward revenue, Credo’s roughly 20x towers over the peer mean near 12x. The premium is real, and the justification rests almost entirely on growth. Credo’s forward two-year revenue CAGR (compound annual growth rate) of around 65% is faster than any large-cap peer in the group. A company growing that fast while holding 68% gross margins earns a richer multiple than a slower compounder.

The risk sits on the other side of that same coin. A multiple built on extraordinary growth punishes any slip toward merely strong. The optical ramp is guided for the back half of fiscal 2027, which means part of the story is still a promise. Supply is the other pressure point. Brennan flagged a looming crunch in 3-nanometer capacity for the 200-gig-per-lane generation, an industry-wide constraint that could cap how fast Credo turns demand into shipped product. A stock near record territory, above its average Street target, has little cushion if either the ramp or the supply slips a quarter.

Credo NTM EV/EBITDA (TIKR)

Credo NTM EV/EBITDA (TIKR)

See how Credo performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $271.95

- Target Price (Mid): ~$720

- Potential Total Return: ~165%

- Annualized Return: ~22% / year

Credo Advanced Valuation Model (TIKR)

Credo Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Credo stock (It’s free!) >>>

Using the mid-case scenario, TIKR’s model points to a target of around $720, a potential total return of around 165%, and an annualized return of around 22% per year over roughly the next five years. The mid case is the honest anchor here because it leans on consensus inputs rather than the most bullish path, and it still clears a strong return.

Two revenue drivers carry the model. The first is the AEC franchise, expanding as neocloud operators join hyperscalers in adopting high-reliability copper links. The second is the optical portfolio, the DSP, silicon photonics, and ZeroFlap lines guided past $600 million in fiscal 2027. The margin driver is operating leverage, with revenue growing faster than the roughly 50% operating-expense growth management guided, pushing net margins toward the high-40s. The primary risk is multiple compression: at around 20x forward revenue, any deceleration in the optical ramp could hit the stock harder than an earnings miss alone would suggest. The upside is a clean optical ramp that validates the $600 million-plus guide and pulls the model’s higher scenarios into view. The downside is a ramp that slips into late fiscal 2027, compressing the multiple, while a near-record price offers little margin of safety.

Conclusion

The new pay package put a number on how management measures its own runway: $2.5 billion in revenue is the first line that matters. The next checkpoint is Credo’s fiscal Q1 2027 report, due September 2, 2026, with revenue guided to $465 million to $475 million. Good looks like a print above $475 million, gross margins holding in the high 60s, and management putting hard early numbers against the $600 million optical goal. Bad looks like a revenue guide-down, a margin slip toward the mid-60s, or optical commentary that quietly pushes the ramp deeper into the year. The first pay tranche needs $2.5 billion in revenue. September tells you whether Credo is tracking toward that line on schedule or whether the board set a bar the business will need longer to clear.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Credo?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Credo, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Credo alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Credo on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Bitcoin Exchange Binance Announces New Listings on its Futures Platform! Here Are the Details

BetOnline Take The Prize Easter Promotion Offers $30k in Cash Prizes!