How should a beginner invest in mutual funds? A clear step-by-step guide

How to start investing in mutual funds: a clear beginner overview

If you are asking how to start investing in mutual funds, begin with the basic idea: a mutual fund pools many investors to buy a portfolio managed to a stated objective, which gives small investors diversification and professional management at scale. This pooled structure makes it practical to own a mix of stocks or bonds without buying each holding yourself, and it is a core reason beginners often choose funds in early saving stages SEC guide to mutual funds.

A mutual fund’s stated objective tells you what the manager will try to do, such as track an index, grow capital, or produce income, and funds are grouped broadly by purpose. Typical categories beginners will see include equity funds that invest in stocks, bond funds that invest in fixed income, balanced funds that mix stocks and bonds, index funds that aim to match a market benchmark, and target-date funds that adjust allocation based on a retirement date.

Mutual funds do not guarantee returns or eliminate risk. Outcomes depend on market moves, the fund’s fees and turnover, the manager’s approach, and how long you stay invested. Be realistic: funds can reduce single-stock risk through diversification, but they still gain or lose value with markets.

Why many beginners ask how to start investing in mutual funds

Beginners often ask this question because mutual funds make diversification and professional management accessible to small accounts, which lowers the entry barrier compared with buying many individual securities FINRA overview on mutual funds.

Industry data also shows strong flows into low-cost index funds and target-date funds, which shapes what options platforms show most prominently and influences what many new investors consider first ICI 2024 Factbook.

These trends matter because the popularity of index mutual funds and target-date funds helps keep simple, low-cost choices widely available. For a beginner, that availability often means you can implement a diversified approach with one or two funds rather than managing many separate positions.

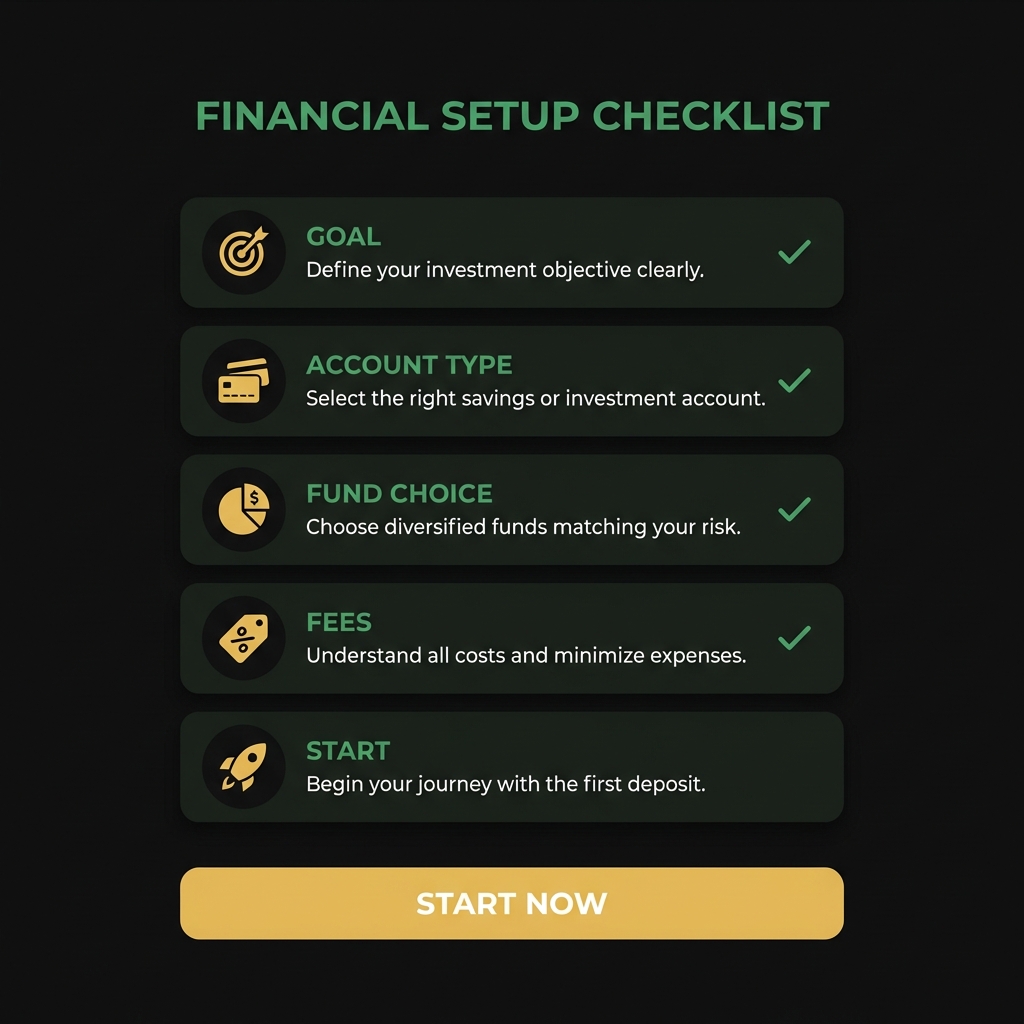

Start by defining your goal and time horizon, compare low-cost funds by expense ratio and objective, choose an appropriate account, and set a simple investment plan such as an automatic contribution or a one-fund starter solution.

Before you pick a fund, think about what you are saving for, how long until you need the money, and how much ups and downs you can tolerate.

Where and how to open an account and buy mutual funds

You can buy mutual funds directly from an asset manager or through a brokerage. Direct purchases sometimes give access to certain share classes or lower minimums, while brokerages offer convenience and consolidated accounts for multiple investments, so compare account rules before you open one Vanguard guide to mutual funds. For a general how to open an account and buy mutual funds guide, see Bankrate’s guide to mutual funds.

Decide whether the fund will sit in a taxable brokerage account or a tax-advantaged account such as an IRA. Account type affects how distributions are taxed, which share classes are available, and sometimes minimum investment rules, so match the account to your goals and tax situation.

Look for automatic investment plans if you prefer steady contributions. Many managers and brokers offer setups that let you transfer the same amount each month into a fund, sometimes called a systematic investment plan or SIP, which can help you keep investing consistently without manual transfers. If you want options for small, regular investing, check our guide to best micro investment apps.

How to choose a mutual fund: practical criteria and a simple checklist

Start with the most quantifiable cost checks: expense ratio and any sales loads. These fees directly reduce net returns over time and are easiest to compare across similar funds, so make them a first screen when narrowing choices FINRA on mutual funds. For how to shop smart about fund costs and fee comparisons see Fidelity’s guide on shopping for funds.

Next review qualitative items such as the fund objective, typical holdings, and turnover. The prospectus and a fund factsheet show what the manager owns and how frequently the portfolio changes; high turnover can increase trading costs and tax events for shareholders.

Also check share classes and platform fees. Different share classes may have different expense ratios or sales charges, and broker platforms can add fees or minimums that change the effective cost of ownership. Make a short comparison table when you have two or three finalists so you can weigh total costs and holdings.

Compare key fund features before you invest

Use this checklist with prospectuses and fund factsheets

When you read a prospectus, look for the stated objective, fee table, and a section on principal risks. A straightforward habit is to note the expense ratio, confirm whether a sales load applies, and scan the top holdings to ensure the fund matches your intended exposure.

How to choose a mutual fund: practical criteria and a simple checklist continued

For many beginners, index mutual funds and low-cost target-date funds are practical first choices because industry flows and product design often make them simple to implement and inexpensive to own relative to many actively managed options ICI 2024 Factbook.

Remember that a lower fee does not automatically make a fund right for your goals, but fees are a durable driver of long-term outcomes and easier to compare than many qualitative traits. Use fees as a filter, then confirm the fund’s objective and holdings match your allocation plan.

Practical investing approaches for beginners: SIPs, lump sum, and simple starter allocations

One practical way to build a position is a systematic investment plan or dollar-cost averaging. Regular contributions spread purchases across market ups and downs and can reduce the risk of poor timing, though historical analysis shows that lump-sum investing has outperformed dollar-cost averaging in many market environments, so neither approach is universally superior Vanguard on investment approaches.

Start with a simple allocation that matches your time horizon. For long-term retirement saving, a mix weighted more to index equity funds can help capture market growth over many years, while a medium-term goal might use a balanced or target-date fund that reduces equity exposure as the date approaches.

Advertise on FinancePolice to reach beginners learning about mutual funds

Sign up for a brief, printable checklist that walks through goal setting, choosing account type, checking fee tables, and scheduling your first automatic transfers.

See advertising and partnership options

Target-date funds offer a one-fund solution for many beginners by automatically adjusting the mix of stocks and bonds as the target date nears. For those who prefer to set and monitor their own allocation, pairing a broad index equity fund with a diversified bond fund is a common, low-cost starting point.

Whichever approach you take, align the strategy with your time horizon, risk tolerance, and saving cadence. Revisit the allocation periodically, especially after major life events or when contributions change.

Tax considerations and mutual fund distributions

Mutual fund distributions include dividends and capital gains, and their tax treatment follows IRS rules. Short-term distributions are typically taxed as ordinary income, while long-term capital gains may be taxed at rates that differ from ordinary income, so check the fund’s tax information and IRS guidance for specifics IRS Topic No. 409 on mutual fund distributions.

Holding the same fund in a tax-advantaged account usually defers or eliminates immediate tax on distributions, while holding it in a taxable account means distributions can create current tax liabilities. That difference affects where you place funds based on your tax and timing objectives.

Funds disclose past distributions and a projection of the tax characteristics you can expect; use those figures as a starting point, but verify current tax rules and your own tax situation before making decisions.

Common beginner mistakes and how to avoid them

A frequent mistake is overlooking the expense ratio and any sales load. Small differences in fees compound over time and reduce your net returns, so compare expense ratios across similar funds before committing Morningstar guide on comparing fees.

Another common error is choosing funds based only on past performance. Past returns are not guarantees of future outcomes, and chasing top short-term performers can increase risk and fees. Focus on consistent strategy, costs, and whether the fund’s holdings match your intended exposure.

Also avoid frequent trading in mutual funds that have transaction fees or redemption rules. If you plan to rebalance or change allocations often, account and fund rules can affect costs, so read the prospectus and platform terms.

Practical examples and short starter portfolios

Example 1, long-term retirement saver: a simple starting point is a broadly diversified index equity fund for most of the growth allocation and a diversified bond fund for stability. Implementation steps include pick the funds, check expense ratios and holdings, choose the account type, and set up automatic contributions.

Example 2, medium-term goal such as a home down payment in five to ten years: a balanced approach with a higher bond allocation than retirement savings reduces volatility and the chance of a large loss close to the need date. Use low-cost index funds for the equity portion and short or intermediate-term bond funds for the fixed-income portion.

Example 3, conservative income preservation: use higher allocation to bond funds or a stable value approach and consider short-duration bond funds to reduce sensitivity to interest rate swings. Target-date funds designed for near-term objectives can also serve conservative goals by shifting toward income assets as the date nears ICI 2024 Factbook.

When you implement any example, track the expense ratios and check distributions periodically, and schedule a review at least once a year to confirm the funds still match your goals.

When you implement any example, track the expense ratios and check distributions periodically, and schedule a review at least once a year to confirm the funds still match your goals.

Wrapping up: next steps and how to keep learning

Before your first purchase, run a short pre-purchase checklist: confirm the goal and time horizon, compare expense ratios and any sales loads, read the prospectus, pick the account type, and set your initial investment amount or automatic plan. This process helps you act with clarity and reduces avoidable surprises SEC guide to mutual funds.

For primary sources and ongoing learning, check official regulator pages, the ICI Factbook for industry trends, fund prospectuses for details, and IRS guidance on distributions, and visit our investing section for related guides.

Yes. Mutual funds pool many investors so small contributions can buy a diversified portfolio; check minimums for the fund or account you choose.

Both are valid. Automatic plans help with regular saving and timing, while lump-sum investing may outperform in some markets. Choose based on comfort with market timing and cash flow.

Expense ratios and any sales loads are key cost factors that reduce net returns over time, so compare them across similar funds before choosing.

References

- https://www.sec.gov/reportspubs/investor-publications/investor-pubs-mutualfundshtm

- https://www.finra.org/investors/learn-to-invest/types-investments/mutual-funds

- https://www.icifactbook.org/2024

- https://financepolice.com/advertise/

- https://financepolice.com/category/personal-finance/

- https://www.nerdwallet.com/investing/learn/how-to-invest-in-mutual-funds

- https://investor.vanguard.com/mutual-funds

- https://www.bankrate.com/investing/guide-to-mutual-funds/

- https://financepolice.com/best-micro-investment-apps/

- https://www.fidelity.com/viewpoints/investing-ideas/how-to-shop-smart

- https://www.irs.gov/taxtopics/tc409

- https://www.morningstar.com/articles/2025/08/14/how-to-invest-in-mutual-funds

- https://financepolice.com/category/investing/

You May Also Like

In ‘Running With Scissors,’ Cavetown learns to accept that risk is in everything

What is the #1 most profitable business? A practical look at passive income business ideas