Starbucks Stock’s Revenue Inflection Is Real. The Margin Recovery Is Where the Upside Hides.

Key Takeaways for Starbucks Stock

- Starbucks posted revenue of $9.53 billion in Q2 FY2026, up 9% year-over-year, its strongest growth rate in eight quarters.

- Operating income grew 22% year-over-year to $0.80 billion, marking the first EPS growth in more than two years.

- Operating margins of 8% remain well below the 16% level the business carried before labor reinvestment began, leaving the recovery’s full profitability upside unpriced.

- TIKR’s model values Starbucks at approximately $136 by late 2030, implying around 34% total return from the current price of $102.

Starbucks stock has posted its first quarter of simultaneous top- and bottom-line growth in more than two years, and the income statement shows the operating leverage story is just beginning. See how far the margin gap still runs on TIKR for free →

Starbucks Stock Posts Back-to-Back Growth for the First Time in Two Years

SBUX Stock Q2 2026 Earnings in USD (TIKR)

SBUX Stock Q2 2026 Earnings in USD (TIKR)

Starbucks Corporation (SBUX) delivered its strongest quarterly revenue growth in eight quarters in Q2 FY2026, reporting $9.53 billion in consolidated net revenues, up 9% year-over-year, while also growing earnings for the first time since early fiscal 2024.

The company operates more than 41,000 coffeehouses globally across company-operated, licensed, and joint venture structures, and has spent the past 18 months rebuilding its operational foundation under CEO Brian Niccol’s “Back to Starbucks” strategy.

North America led the quarter, with comparable store sales growing 7%, driven by more than 4 percentage points of transaction growth.

Niccol noted that morning visit levels in the U.S. are “roughly back to fiscal 2022 levels,” a milestone that signals the operational rebuild is gaining traction across the most important daypart.

The delivery channel contributed as well, growing more than 30% year-to-date across U.S. company-operated locations.

All ten of Starbucks’ top international markets, including China, delivered positive comparable sales for the first time in nine quarters.

Niccol described the trajectory plainly in Q2 earnings call: “Q2 marked a milestone for the business. We delivered growth on both the top and bottom line for the first time in more than 2 years.”

Starbucks raised its fiscal 2026 guidance to global comparable sales growth of 5% or better, and its EPS range now stands at $2.25 to $2.45.

The company’s 90-day active Starbucks Rewards membership reached 35.6 million members, up 4% year-over-year, bucking the typical seasonal decline in Q2.

The turnaround story is in the transcript. The income statement shows whether the margin math supports it. Pull up the SBUX financials on TIKR and check the operating leverage trajectory for free →

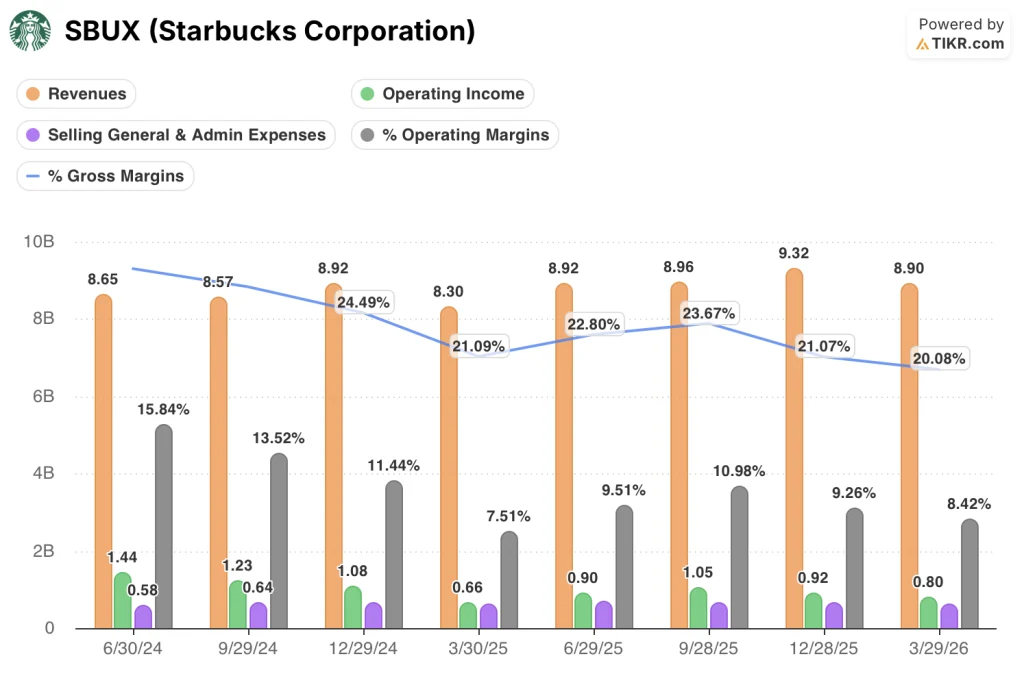

Starbucks’ Operating Margins at 8%: The Gap Between Revenue Recovery and Profit Recovery

SBUX Stock Quarterly Financials (TIKR)

SBUX Stock Quarterly Financials (TIKR)

Starbucks’ operating margins stood at 8% in Q2 FY2026, up from a trough of 8% in the prior-year period, but still less than half the 16% the business carried in Q3 FY2024 before the Green Apron Service labor investments began flowing through the P&L.

Revenue grew 9% year-over-year to $9.53 billion, the strongest growth rate across the eight quarters shown in the income statement.

Gross margins compressed to 20%, down from 23% in the year-ago quarter, as product cost inflation, tariff-related pressures, and innovation-led mix shift in food pushed cost of goods sold higher faster than revenue recovered.

Operating income reached $0.80 billion, a 22% year-over-year improvement, demonstrating that operating leverage is beginning to emerge even as gross margin compression persists at the top of the P&L.

SG&A declined 6% year-over-year as organizational streamlining reduced support center headcount, and management confirmed the $2 billion cost savings program remains on track through fiscal 2028.

The thesis tension is explicit in the data: revenue is recovering at 9% while gross margins are still contracting, which means the operating income recovery is being driven almost entirely by cost discipline below the gross profit line, not by pricing power recovering at the top.

Starbucks Runs at 8% Operating Margins While MCD Holds 44% and QSR Sits at 26%

SBUX Stock Operating Margins vs MCD Stock and QSR Stock (TIKR)

SBUX Stock Operating Margins vs MCD Stock and QSR Stock (TIKR)

Starbucks posted an 8% operating margin in the most recent quarter, while McDonald’s (MCD) ran at 44% across the same period.

Restaurant Brands International’s (QSR) operating margin stood at 26% in the most recent quarter, itself more than three times Starbucks’ current level.

The gap between Starbucks and both peers has been persistent across the full eight-quarter window shown, not a product of the most recent quarter’s cost pressures.

McDonald’s margins have held in a range between 45% and 47% through the same period when Starbucks fell from 16% to a trough of 8%.

The peer data makes the recovery thesis legible in a different way than the income statement alone: Starbucks is not trying to match McDonald’s franchise-model economics, but the distance from QSR’s 26% shows how much operating income the business is leaving unrealized at current cost structure levels.

Restaurant Brands International’s 26% margin was itself achieved through a largely licensed and franchised model, similar to the direction Starbucks is moving internationally as its own license mix approaches 90%.

The structural implication is that as Starbucks completes its transition to a near-fully licensed international portfolio, the cost base that currently suppresses margins should compress, and the peer chart shows the range of outcomes that model can produce.

Is Starbucks Stock Undervalued in 2026? TIKR’s $136 Model Sets the Condition

TIKR’s model values Starbucks at approximately $136 by late 2030, implying around 34% total return from the current price of approximately $102, or roughly 7% per year.

SBUX Stock Valuation Model Results (TIKR)

SBUX Stock Valuation Model Results (TIKR)

The credibility of that target rests on a single income statement condition: operating margins recovering from 8% toward the level the business demonstrated before the labor reinvestment cycle began.

The cost structure is already moving in the right direction, with SG&A contracting and the $2 billion savings program providing a multi-year tailwind that has yet to fully show up in operating income.

If gross margins stabilize as coffee price pressures moderate in the back half of fiscal 2026, the combined effect of revenue operating leverage and cost savings creates a compound path to meaningfully higher operating income without requiring top-line heroics.

Run TIKR’s full valuation model on SBUX yourself and see what margin assumptions drive the $136 target on TIKR for free →

Should You Invest in Starbucks Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Starbucks Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Starbucks Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SBUX stock on TIKR for Free →

What Did Starbucks Say About Its $2 Billion Cost Savings Program?

CFO Cathy Smith confirmed the $2 billion gross savings program remains on track through fiscal 2028, with savings split across product and distribution costs, operating expenses, and G&A, though much of the near-term benefit is currently offsetting Green Apron Service investments.

Ayrıca Şunları da Beğenebilirsiniz

Fed Governor Calls For Strong Stablecoin Oversight As CLARITY Act’s Final Text Gets Delayed

Startup Investor Secret Deal Room – Monte Carlo

$280M drained via social engineering

Popüler Haberler

Daha fazla